How We Save Money for Travel (and other financial goals)

“Stay inside and have no fun ever while searching for pennies in the couch until you reach your goal”

Ok maybe not quite that, but generally the tips are to basically cut out all the fun things in your life…which will end up being for like 2 weeks until it becomes too hard and you blow all the money you saved on a massive online shopping spree while drinking a good bottle of wine and eating your favourite takeaways (just me?).

Saving money (or even just having enough to cover costs) is hard and something I struggled with for YEARS so I’m going to let you guys know what we do to save money for these incredible trips we take (and we do pay for them all ourselves – no sponsored trips here!).

But first, a bit of history

When I went on my big OE to New Zealand and Australia, I had saved up most of what I needed but relied on a credit card and student loan to pay for my course and time in Australia. This was before I knew about exchange rates and how they can turn against you very quickly – my trip got A LOT more expensive in Canadian dollar terms between booking it and actually paying for everything.

I got back to Canada in debt and it took a little bit of time to find work. What I did find didn’t pay very well and I was living in Vancouver (because moving back to my small hometown was too much for my prideful 19 year old self to handle) so things were a bit tight and I again relied on my credit card and loan to get through.

Even then I had the attitude that experiences are more important than money and I’m super impatient so I put a very expensive one way flight to New Zealand on my credit card to live with this dude I had spent a few days with the year before.

(Why didn’t my parents protest? Cause they’re awesome. That’s why. And in their defence we did end up getting married a few years later.)

Look at how young we were!

Cutting a long story short, a few years and thousands of “I’ll just put it on the card and worry about it later”’s, Matt and I decided to move to London and spend 2 months travelling around South East Asia on the way there.

With all our research on travel costs and making sure you have enough to afford setting up life in London, I worked out that I needed $10,000. I was $5,000 in the red. And we were leaving in a year.

But by the time we left for London, I was out of debt, had saved $10,000, and FINALLY got a grip on my finances.

So, how did I save enough to get out of debt and afford to travel?

By getting into one simple habit – I recorded every single penny I spent. Every day, no excuses. I’ll admit it was really hard to start but I had a spreadsheet on a USB that I carried everywhere in my purse (this was before the days of apps and Google Sheets where you could access them on the go) – when I was at work, I was able to input any money I spent at lunch straight away so I didn’t forget and very quickly I got into the habit of recording every penny.

Once I started seeing where my money was going, I was able to make smarter decisions about my spending. Even just knowing that I would have to input a purchase into my spreadsheet was enough to make me stop and think ‘do I really need this?’

The results were eye-opening – getting a coffee every day didn’t seem like a big expense but when I added those coffees up it was $15 a week, or $780 a year.

Not only did tracking everything help curb my spending on random items, it gave me the ability to actually create a budget which is one of the tips you find in those rubbish saving money articles. Just make a budget and stick to it! Well, how can I make a budget if I don’t know what I spend? You can’t!

Write down your spending first and then look at creating a budget to stick to. Don’t base your budget off some hypothetical numbers in an article; use your actual spending as a starting point.

Some people will say they don’t earn enough money to get out of debt or save. They can’t save anything until they earn more money. Sometimes that might be true but most of the time it is just the easy answer. There is a huge correlation between spending and income naturally and we’ve found it can be easy to relax as income increases and see all that hard work go to waste on buying more and more creative and stupid things. Whether you earn minimum wage or a six figure salary, the same rules apply.

But I hate spreadsheets, I don’t think this is for me….

Well, then I feel bad for you. Spreadsheets are awesome! But I kinda get it. This is the part where I admit I hated spreadsheets when I first started tracking my spending. But they aren’t hard to get the hang of.

We were using a spreadsheet at home up until the beginning of this year. We started getting a bit lazy with inputting transactions because it was on our home computer and not on us all the time (and we just couldn’t be bothered looking at another spreadsheet at the end of a long day at work spent….staring at spreadsheets).

We’d go a week without tracking anything and it would mean a lot of time, and just fudging our amounts under “Misc” instead of figuring out what we actually spent the money on. It also meant we were spending money on everything without giving it much thought. Not having a firm handle on our finances was getting stressful again. Not being accountable meant we were throwing away money far too easily on things we didn’t really need.

So we switched to Goodbudget so we could input transactions as they happen and have saved hundreds of £ because of it. Goodbudget is simple with great Android and iOS apps as well as website access. It is based on the old school method of putting your pay straight into different envelopes (e.g. Rent, Groceries, Phone etc). There’s a free version and a premium version – the free one will work just fine for most people and should be good for just starting out but if you have a lot of accounts then go for the premium option (@ $45 a year). There are heaps of other apps out there as well.

We’ve since discovered Google sheets (a great place to get a simple (and free!) budget template to start with) which we can both access while on the go. We’ll likely have to switch to using that in the future as Goodbudget doesn’t support multiple currencies, but for now, it does the trick.

So what are the main lessons I learned?

1 – Track your Spending!

This is the most important one. Once you start recording your spending, you’ll be able to work out where your money goes and exactly how much you can save each month towards your goal based on that spending. If that amount saved isn’t high enough then you’ve got all the information you need to identify where you can cut extra spending from. For us, travel is a priority so we have a set amount that goes into a separate account each month. Because we know our spending habits, we’ve made it a reasonable number that we know we can save (and not touch) which means no more feeling crap that we’ve dipped into our travel savings to pay for groceries or a meal out.

2 – Small Changes = Big Savings

You’ll quickly start to see that small changes to regular items have the biggest impact.

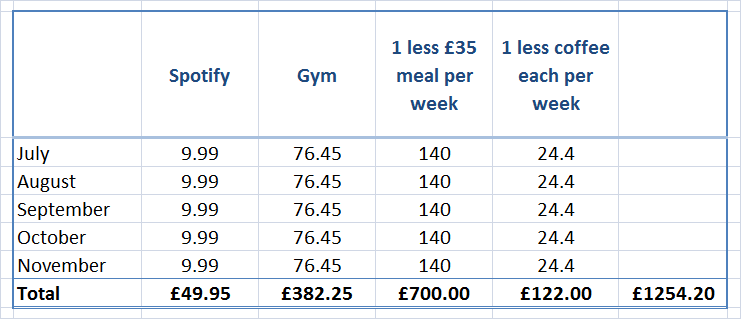

Matt and I are currently tightening up our spending for our own big goal (more on this later) so we had a look at what we’ve been spending money on and noticed that doing the following things would save us heaps over the next few months.

The gym is a hard one to cancel as we’re also in the middle of a big drive to get fit and healthy as well but this will be replaced with walking to and from work (which also saves on transport costs – another £500 just from Matt not taking the Tube!) and doing at home workouts. Instead of saying we’re never going out for food or coffee again, we just need to reduce it by one meal/coffee a week to save quite a bit of money! You don’t need to skip every single fun thing in your life to have it make a difference.

It adds up quickly and the only way you’ll see it is if you track every penny you spend. It’s hard to get started, but you’ll be so glad you did!

Aside from making small changes there are obviously some big expenses that have a huge impact on your budget. Mike and Lauren (who we follow on Youtube) have a great (and much more frugal and creative) approach to saving (their goal being a very early retirement). This video is great at highlighting some creative ways to save money on the “3 Biggest Budget Busters” (housing, transportation and food).

3 – Think of the Opportunity Cost (this is our favourite one)

Relate what you’re spending to actual travel costs from your dream trip.

For example, one coffee in London is a whole meal in Thailand. If you get takeaways or have dinners out, skipping one will then fund your entrance fee to Alcatraz or another similar attraction. Saving £1,254.20 on things you don’t really need could be your main trunk flights or an extra month of travel in South East Asia (or it would fund a large chunk of whatever else it is you’re saving for).

More money for foreign delicacies

4 – Set Goals

Just like almost anything else in life, you need to set goals, write them down and review how you’re doing against them regularly. The goal needs to be ambitious but achievable – there’s no point in aiming to save £100k this year if that isn’t reasonably possible.

Work out how much you could save if you were perfect then multiply that number by 80-90% to allow yourself a buffer for unexpected expenses (new car tyre, replacement phone etc).

The other thing to do with financial goals is to link it to that actual end goal. It’s unlikely you want to save £10k to pile it up on your bed and look at it (or maybe it is). If your goal is to save £10k for your perfect wedding then target your goal at that not at saving £10k. Name it your Wedding Fund and keep thinking about how all the sacrifices now will one day go towards that dream wedding…which links well into number 5.

5 – Open a Separate Bank Account for Your Goal

Most banks will be perfectly happy to open another savings account for you free of charge and with online banking and apps like Goodbudget you can then name your account after whatever your goal is. So that boring savings account becomes the “Wedding Fund” or “Thailand Fund”.

I’d also recommend researching the available accounts and using the right type of account that will maximise your interest and allow for at least some form of lock up. Regular Saver accounts here in the UK are perfect for that (you put away £250 per month or similarly small amount and don’t get the total back until 12 months after account opening and you get a higher interest rate than in nearly any other account type available).

Pin it!

{kind=link}

Good post! Have you heard of Pocketsmith? It’s great – it pulls transactions from all of your bank accounts and you can categorise from there. We’ve found this really easy and useful for tracking where we actually spend our money.

I hadn’t! Just checked it out and love that it lets you sync accounts as well as multiple currencies! Too bad it doesn’t have a mobile app (that I could find) and it’s a bit expensive – we’ll definitely keep it in mind though. Thanks!

Great tips; I totally agree with tracking your spending, we do this too and it would be impossible to save if we didn’t. I’ll have to check out the resources you use for this as we do ours manually on a spreadsheet which probably isn’t the easiest option – when we’re actually travelling we use the Trail Wallet App, which is awesome. It’s a pain, but we also end up changing our savings account every year to get the best interest rates, it’s worth it though when you see that you can earn a couple of hundred pounds from it per year.

I would love to be able to use the Trail Wallet App but they don’t have an Android app 🙁 We’re looking at changing banks/savings accounts at the moment too. Who do you use?

I use a free online accounting program from Canada – Wave. It is very basic, and designed for small business, but they have the option to track your personal money as well. And the free version has all the bells and whistles they have. They can upload directly from your bank, but that had glitches for me so I upload them monthly with the bank statement. It also has a budget tool, but not so good on the smartphone apps. And being free they are slow on the development. But it works really well for my needs.

Thanks Steve! Looks good – just missing an app for us!

Nice practical and, more importantly, feasible tips! I’d add that the more you cut back on small things, the more you’ll realize that you don’t actually need them and you can live with a lot less… but I agree with not cutting out all the fun in your life! 🙂

Absolutely! I’ve cut way back on the amount of coffees I buy and don’t really miss them. Making them at home or work is much cheaper!

Very helpful article. Traveling will cost you a lot, if you are unprepared and under-researched on the itinerary. So creating a savings plan can surely help anyone avoid this traveling troubles. By the way, thank you so much for these practical tips. Good job for this.